Tweet

Tweet

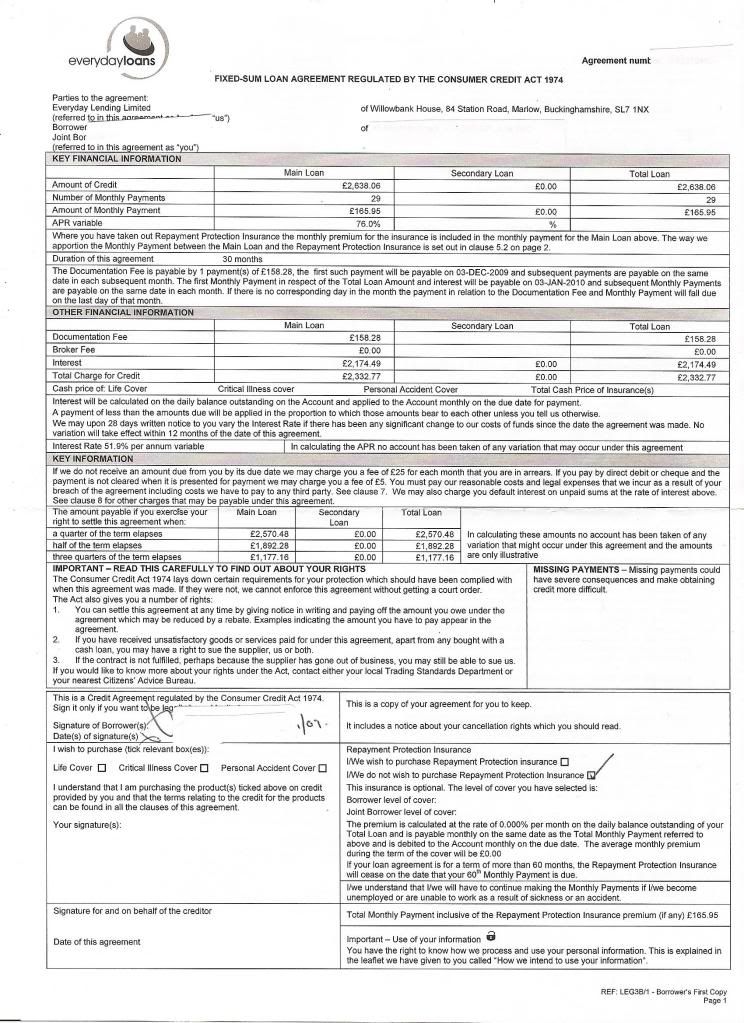

Hi,

I started a debt management plan 1 year ago with KFM. All my creditors accepted this although Everyday loans refused initially to agree to payments. However they have been recieving Ł35 a month off of a Ł2500 loan. In their recent statement from them they show all the payments but the loan debt has now increased to Ł4,000. KFM state via phone that Everyday loans have agreed to the payment terms. However I cannot seem to get this in writing.

If this continues I will owe nearly Ł15,000 by the time the plan ends which is more than all my debts together.

I have tried discussing this with the loan company who state that unless i make full payments as in the loan agreement this will be the case.

The debt management company state that the loan company have agreed reduced payments and the letter they sent me is a standard letter!

As I don't have written confirmation of this I am worried that by the end of my debt management plan I will be worse off because of this one company. Would I then be able to take this to the financial ombudsman or would i end up having to pay. I cannot seem to get an answer from the debt management company!

I started a debt management plan 1 year ago with KFM. All my creditors accepted this although Everyday loans refused initially to agree to payments. However they have been recieving Ł35 a month off of a Ł2500 loan. In their recent statement from them they show all the payments but the loan debt has now increased to Ł4,000. KFM state via phone that Everyday loans have agreed to the payment terms. However I cannot seem to get this in writing.

If this continues I will owe nearly Ł15,000 by the time the plan ends which is more than all my debts together.

I have tried discussing this with the loan company who state that unless i make full payments as in the loan agreement this will be the case.

The debt management company state that the loan company have agreed reduced payments and the letter they sent me is a standard letter!

As I don't have written confirmation of this I am worried that by the end of my debt management plan I will be worse off because of this one company. Would I then be able to take this to the financial ombudsman or would i end up having to pay. I cannot seem to get an answer from the debt management company!

Comment